Modelling Probability of Loan Default

When banks and other financial institutions evaluate a loan request, they must ascertain the risk of default. Defaults can be very costly to banks and predictive analytics can be deployed to help banks make the right decisions. This project involves using a past Kaggle competition to model default of a customer based on many different features.

Data Exploration

The dataset comprises over 300,000 customers with over 100 features; it is quite a large dataset packed with data. Let's try to make sense of it. It gives demographic and financial information of a customer and then says if he/she defaulted on a loan.

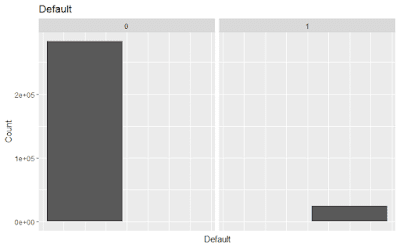

Let's first get a broad-level overview of the fraction of defaults.

The bank issues both cash loans and revolving loans. The latter are flexible loans and are rather open-ended. Let us see how default rates vary based on the type of loan.

It seems that a smaller proportion of revolving loans, as opposed to cash loans, suffer from default. This makes intuitive sense as revolving loans are more likely to be issued to more trustworthy borrowers.

We want to identify if there is any relation between income, the amount of credit, and default.

Interestingly, there does not appear to be any such relationship. Here, the red circles are customers who defaulted and they seem to be well mixed-in with the blue circles, those who did not default.

Data Cleaning

I convert some of the categorical variables, such as gender and binaries for car and home ownership to numeric to make analysis easier.

It is important to explore various columns to check for anomalies.

The age column looks like this:

Min. 1st Qu. Median Mean 3rd Qu. Max.

-25229 -19682 -15750 -16037 -12413 -7489

Clearly, this needs to be fixed. We just need to divide by -365 to get the age in years. We then round down to get the age in years.

The column for days employed is also anomalous. There is one outlier value which has been inputted for many records.

Test data

We split the data into the training set, which will be used to create the models, and the best model will be decided based on how well it predicts the test data. The training data comprises the first 70% of the data (the first 215257 records) and the remaining 30% is the testing data.

Model 1: Logistic Regression

My first model is logistic regression. The features selected along with their coefficients are at the end of the post as they look quite ugly...

Model 1: Logistic Regression

My first model is logistic regression. The features selected along with their coefficients are at the end of the post as they look quite ugly...

While most variables are significant, this model is clearly not optimal, given the R-squared value of just over 5%. I use this model to predict the test data (the remaining 30% of our observations).

Explaining the Variables

Most, but not all, variables included in the model are statistically significant, at least at the 10%. The initial variables include the type of loan and a binary for car ownership, which are as expected. Interestingly, home ownership was not significant as a determinant of the probability of default, when other factors are accounted for.

With regards to family status, the baseline was civil marriage and it seems that every other family profile has a lower probability of default on average than civil marriage. The HOUR_APPR_PROCESS_START variable refers to the time the loan application was initiated, presumably online, with 0 (12AM) as the baseline. It is interesting to note that this variable is significant for almost all hours; it appears that those who begin their applications at midnight are the riskiest borrowers.

Many occupation factors are significant; here, the baseline is the Unknown category, and relatively higher-paying occupations are less risky. There is likely a correlation with income here, and since income was insignificant, it is not in the model.

Location variables are also important here; those who live, work, and register their application for the loan in the same city are the safest applicants.

There is no information on what each document is so it is impossible to make any conclusions on what the documentary evidence of a loan application can tell about the applicant's probability of default.

The older the person is and the longer they have worked, the safer they are. There is also an interaction for age and years worked included to highlight the non-linearity.

Performance of Model

Given the low explanatory power of the model, it is not surprising that the model did not perform very well on the test data. This graphic conveys this finding.

Model 2: K-Nearest Neighbours

There are alternatives to logistic regression which can be tried, for example, k-nearest neighbours.

I use the same variables as in the above case, however, all are now numerically coded.

Using the 20 nearest neighbours to predict the outcome, I predict whether a customer will default based on the given features. This is the outcome contingency matrix.

Actual_Outcome

Predicted_Outcome 0 1

0 63687 5492

1 5160 966

In this case, k-nearest neighbours has also not given very good results. In particular, there is a very high false positive rate. Of all the predicted customer defaults, only 15.8% of customers actually default. Meanwhile, of all the customers who are not predicted to default, 7.9% actually default; this is not a good result given the very low base rate of non-defaulters.

Conclusion

In this case, neither logistic regression nor k-nearest neighbours have provided satisfactory results. This could be due to a variety of reasons. One, the data may not be relevant enough for the purpose of predicting the probability of default. A second reason could be improper variable selection from the available data.

This exercise gives insight into the complexity of tasks for a financial institution while deciding whether to issue a loan. There are many factors which can influence a customer's probability of default and banks have to maintain lots of data to build reliable models to use for their decision-making.

Appendix: Coefficients from the Regression

(Intercept)

-0.79595

NAME_CONTRACT_TYPERevolving loans***

-0.18317

FLAG_OWN_CAR***

-0.26606

FLAG_OWN_REALTY

-0.01833

REGION_RATING_CLIENT***

0.355928

FLAG_WORK_PHONE***

0.258398

AMT_CREDIT***

2.79E-06

AMT_ANNUITY***

1.11E-05

AMT_GOODS_PRICE***

-3.57E-06

NAME_FAMILY_STATUSMarried***

-0.13747

NAME_FAMILY_STATUSSeparated

-0.04431

NAME_FAMILY_STATUSSingle / not married

-0.00917

NAME_FAMILY_STATUSWidow***

-0.29511

factor(HOUR_APPR_PROCESS_START)1.

-1.33273

factor(HOUR_APPR_PROCESS_START)2.

-0.92361

factor(HOUR_APPR_PROCESS_START)3*

-1.21312

factor(HOUR_APPR_PROCESS_START)4*

-1.17613

factor(HOUR_APPR_PROCESS_START)5*

-1.09525

factor(HOUR_APPR_PROCESS_START)6*

-0.99523

factor(HOUR_APPR_PROCESS_START)7*

-1.01898

factor(HOUR_APPR_PROCESS_START)8*

-1.03462

factor(HOUR_APPR_PROCESS_START)9*

-1.06499

factor(HOUR_APPR_PROCESS_START)10*

-1.08422

factor(HOUR_APPR_PROCESS_START)11*

-1.0546

factor(HOUR_APPR_PROCESS_START)12*

-1.06202

factor(HOUR_APPR_PROCESS_START)13*

-1.07317

factor(HOUR_APPR_PROCESS_START)14*

-1.06996

factor(HOUR_APPR_PROCESS_START)15*

-1.06118

factor(HOUR_APPR_PROCESS_START)16*

-1.12422

factor(HOUR_APPR_PROCESS_START)17**

-1.2677

factor(HOUR_APPR_PROCESS_START)18*

-1.15939

factor(HOUR_APPR_PROCESS_START)19*

-1.02128

factor(HOUR_APPR_PROCESS_START)20*

-1.1636

factor(HOUR_APPR_PROCESS_START)21*

-1.24743

factor(HOUR_APPR_PROCESS_START)22

-0.8558

factor(HOUR_APPR_PROCESS_START)23

-1.16614

FLAG_CONT_MOBILE.

-0.35471

FLAG_PHONE***

-0.10984

CNT_FAM_MEMBERS

0.001569

OCCUPATION_TYPEAccountants***

-0.25952

OCCUPATION_TYPECleaning staff*

0.133099

OCCUPATION_TYPECooking staff*

0.115596

OCCUPATION_TYPECore staff***

-0.15884

OCCUPATION_TYPEDrivers***

0.336836

OCCUPATION_TYPEHigh skill tech staff**

-0.163

OCCUPATION_TYPEHR staff

-0.0928

OCCUPATION_TYPEIT staff

-0.02068

OCCUPATION_TYPELaborers***

0.21998

OCCUPATION_TYPELow-skill Laborers***

0.534507

OCCUPATION_TYPEManagers

0.02606

OCCUPATION_TYPEMedicine staff*

-0.11466

OCCUPATION_TYPEPrivate service staff*

-0.24476

OCCUPATION_TYPERealty agents

-0.15031

OCCUPATION_TYPESales staff

0.008537

OCCUPATION_TYPESecretaries

-0.14882

OCCUPATION_TYPESecurity staff***

0.244169

OCCUPATION_TYPEWaiters/barmen staff

0.12137

LIVE_CITY_NOT_WORK_CITY*

0.240491

REG_CITY_NOT_WORK_CITY***

0.196464

FLAG_DOCUMENT_3***

0.219586

DEF_30_CNT_SOCIAL_CIRCLE***

0.210821

FLAG_DOCUMENT_2***

2.853055

FLAG_DOCUMENT_5**

0.227776

FLAG_DOCUMENT_13**

-0.61187

FLAG_DOCUMENT_11**

-0.39757

FLAG_DOCUMENT_14***

-0.92517

FLAG_DOCUMENT_15*

-0.91468

FLAG_DOCUMENT_16***

-0.60078

FLAG_DOCUMENT_18***

-0.4145

AGE***

-0.01692

YEARS_WORK***

-0.06549

UNACCOMPANIED**

0.0732

HIGHER_ED***

-0.41263

YEARS_LAST_PHONE_CHANGE***

-0.07162

ACADEMIC_DEGREE.

-0.97827

FLAG_OWN_CAR:FLAG_OWN_REALTY**

0.083924

LIVE_CITY_NOT_WORK_CITY:REG_CITY_NOT_WORK_CITY**

-0.33224

AGE:YEARS_WORK***

0.000624

Source of dataset from kaggle - https://www.kaggle.com/c/home-credit-default-risk/data

Explaining the Variables

Most, but not all, variables included in the model are statistically significant, at least at the 10%. The initial variables include the type of loan and a binary for car ownership, which are as expected. Interestingly, home ownership was not significant as a determinant of the probability of default, when other factors are accounted for.

With regards to family status, the baseline was civil marriage and it seems that every other family profile has a lower probability of default on average than civil marriage. The HOUR_APPR_PROCESS_START variable refers to the time the loan application was initiated, presumably online, with 0 (12AM) as the baseline. It is interesting to note that this variable is significant for almost all hours; it appears that those who begin their applications at midnight are the riskiest borrowers.

Many occupation factors are significant; here, the baseline is the Unknown category, and relatively higher-paying occupations are less risky. There is likely a correlation with income here, and since income was insignificant, it is not in the model.

Location variables are also important here; those who live, work, and register their application for the loan in the same city are the safest applicants.

There is no information on what each document is so it is impossible to make any conclusions on what the documentary evidence of a loan application can tell about the applicant's probability of default.

The older the person is and the longer they have worked, the safer they are. There is also an interaction for age and years worked included to highlight the non-linearity.

Performance of Model

Given the low explanatory power of the model, it is not surprising that the model did not perform very well on the test data. This graphic conveys this finding.

Model 2: K-Nearest Neighbours

There are alternatives to logistic regression which can be tried, for example, k-nearest neighbours.

I use the same variables as in the above case, however, all are now numerically coded.

Using the 20 nearest neighbours to predict the outcome, I predict whether a customer will default based on the given features. This is the outcome contingency matrix.

Actual_Outcome

Predicted_Outcome 0 1

0 63687 5492

1 5160 966

In this case, k-nearest neighbours has also not given very good results. In particular, there is a very high false positive rate. Of all the predicted customer defaults, only 15.8% of customers actually default. Meanwhile, of all the customers who are not predicted to default, 7.9% actually default; this is not a good result given the very low base rate of non-defaulters.

Conclusion

In this case, neither logistic regression nor k-nearest neighbours have provided satisfactory results. This could be due to a variety of reasons. One, the data may not be relevant enough for the purpose of predicting the probability of default. A second reason could be improper variable selection from the available data.

This exercise gives insight into the complexity of tasks for a financial institution while deciding whether to issue a loan. There are many factors which can influence a customer's probability of default and banks have to maintain lots of data to build reliable models to use for their decision-making.

Appendix: Coefficients from the Regression

(Intercept)

-0.79595

NAME_CONTRACT_TYPERevolving loans***

-0.18317

FLAG_OWN_CAR***

-0.26606

FLAG_OWN_REALTY

-0.01833

REGION_RATING_CLIENT***

0.355928

FLAG_WORK_PHONE***

0.258398

AMT_CREDIT***

2.79E-06

AMT_ANNUITY***

1.11E-05

AMT_GOODS_PRICE***

-3.57E-06

NAME_FAMILY_STATUSMarried***

-0.13747

NAME_FAMILY_STATUSSeparated

-0.04431

NAME_FAMILY_STATUSSingle / not married

-0.00917

NAME_FAMILY_STATUSWidow***

-0.29511

factor(HOUR_APPR_PROCESS_START)1.

-1.33273

factor(HOUR_APPR_PROCESS_START)2.

-0.92361

factor(HOUR_APPR_PROCESS_START)3*

-1.21312

factor(HOUR_APPR_PROCESS_START)4*

-1.17613

factor(HOUR_APPR_PROCESS_START)5*

-1.09525

factor(HOUR_APPR_PROCESS_START)6*

-0.99523

factor(HOUR_APPR_PROCESS_START)7*

-1.01898

factor(HOUR_APPR_PROCESS_START)8*

-1.03462

factor(HOUR_APPR_PROCESS_START)9*

-1.06499

factor(HOUR_APPR_PROCESS_START)10*

-1.08422

factor(HOUR_APPR_PROCESS_START)11*

-1.0546

factor(HOUR_APPR_PROCESS_START)12*

-1.06202

factor(HOUR_APPR_PROCESS_START)13*

-1.07317

factor(HOUR_APPR_PROCESS_START)14*

-1.06996

factor(HOUR_APPR_PROCESS_START)15*

-1.06118

factor(HOUR_APPR_PROCESS_START)16*

-1.12422

factor(HOUR_APPR_PROCESS_START)17**

-1.2677

factor(HOUR_APPR_PROCESS_START)18*

-1.15939

factor(HOUR_APPR_PROCESS_START)19*

-1.02128

factor(HOUR_APPR_PROCESS_START)20*

-1.1636

factor(HOUR_APPR_PROCESS_START)21*

-1.24743

factor(HOUR_APPR_PROCESS_START)22

-0.8558

factor(HOUR_APPR_PROCESS_START)23

-1.16614

FLAG_CONT_MOBILE.

-0.35471

FLAG_PHONE***

-0.10984

CNT_FAM_MEMBERS

0.001569

OCCUPATION_TYPEAccountants***

-0.25952

OCCUPATION_TYPECleaning staff*

0.133099

OCCUPATION_TYPECooking staff*

0.115596

OCCUPATION_TYPECore staff***

-0.15884

OCCUPATION_TYPEDrivers***

0.336836

OCCUPATION_TYPEHigh skill tech staff**

-0.163

OCCUPATION_TYPEHR staff

-0.0928

OCCUPATION_TYPEIT staff

-0.02068

OCCUPATION_TYPELaborers***

0.21998

OCCUPATION_TYPELow-skill Laborers***

0.534507

OCCUPATION_TYPEManagers

0.02606

OCCUPATION_TYPEMedicine staff*

-0.11466

OCCUPATION_TYPEPrivate service staff*

-0.24476

OCCUPATION_TYPERealty agents

-0.15031

OCCUPATION_TYPESales staff

0.008537

OCCUPATION_TYPESecretaries

-0.14882

OCCUPATION_TYPESecurity staff***

0.244169

OCCUPATION_TYPEWaiters/barmen staff

0.12137

LIVE_CITY_NOT_WORK_CITY*

0.240491

REG_CITY_NOT_WORK_CITY***

0.196464

FLAG_DOCUMENT_3***

0.219586

DEF_30_CNT_SOCIAL_CIRCLE***

0.210821

FLAG_DOCUMENT_2***

2.853055

FLAG_DOCUMENT_5**

0.227776

FLAG_DOCUMENT_13**

-0.61187

FLAG_DOCUMENT_11**

-0.39757

FLAG_DOCUMENT_14***

-0.92517

FLAG_DOCUMENT_15*

-0.91468

FLAG_DOCUMENT_16***

-0.60078

FLAG_DOCUMENT_18***

-0.4145

AGE***

-0.01692

YEARS_WORK***

-0.06549

UNACCOMPANIED**

0.0732

HIGHER_ED***

-0.41263

YEARS_LAST_PHONE_CHANGE***

-0.07162

ACADEMIC_DEGREE.

-0.97827

FLAG_OWN_CAR:FLAG_OWN_REALTY**

0.083924

LIVE_CITY_NOT_WORK_CITY:REG_CITY_NOT_WORK_CITY**

-0.33224

AGE:YEARS_WORK***

0.000624

Source of dataset from kaggle - https://www.kaggle.com/c/home-credit-default-risk/data

Comments

Post a Comment